8 entrepreneurial views on investing in venture capital

"I am a better investor because I am a businessman, and I am a better businessman because I am an investor." Warren Buffett

Introduction

To build or guide startups optimally, one must think and strategize as an investor. Management and operational skills are fundamental, but understanding barriers to entry and unit economics, as well as foreseeing structural shifts in technology, are indispensable to steer the ship in the right direction. Consequently, to be a superior startup investor, it is crucial to have also been previously entrenched with other fellow entrepreneurs to better calibrate bullshit from reality. Numbers in spreadsheets and graphs in presentations drafted solely by investors may be coherent in the boardroom but lose viability when they hit the ground.

Through wisdom imparted by some of the most successful players in startup investment; this article serves as a comprehensive overview on investing in startups, accessible to first-time investors and valuable for experienced entrepreneurs. The idea is for you to have a single go-to document that deep dives into the essential facets to consider before investing in a startup.

*There is also a section at the end of the article with additional reading materials, notes, graphs, and other resources.

Have an Unfair Advantage

Before analyzing any investment opportunity, make sure that you have an unfair advantage in terms of industry insights or access to opportunities. Ask yourself: what do I understand that other people don’t? If you do not have an answer to this question, you do not have a competitive edge. Three factors can give you an unfair advantage:

Domain expertise:

You have an understanding of structural shifts that are occurring within an industry that will create future business opportunities. Examples include Moore's law in software, Metcalfe's law in regards to network effects such as in social media, or the Power law in modern marketplace businesses like Airbnb.

Leveraging networks:

You can identify network connections you or your co-investors in a particular investment opportunity. For instance, other companies in your investment portfolio who have synergies and/or can structure deals that can give the company exclusivity or cheaper access to a platform, product, or other resources.

Access to deals: Leveraging future capital

You have privileged access to a deal through a personal connection with an investor or entrepreneur, and you can get the same deal terms that a large fund has except you are investing less cash. Early deal terms with pro-rata rights can be later executed on the next round through a syndicate of other investors, giving you the ability to charge a carry fee on the follow-on investment to outside investors.

Take away:

If you cannot regurgitate your unfair advantage to a friend who wants to learn about the investment opportunity, you are not investing, you are speculating. In the words of legendary investor Peter Lynch: “Know what you own, and know why you own it.” If you cannot answer why you want to own the stock, study the opportunity further or pass on the investment.

* Important assumption: For simplicity purposes, I am assuming you will be using a tag-along investment strategy. In other words, you will be investing in startups that are being analyzed by other venture capital firms, seasoned angel investors, or other professional investors. You are investing alongside them and are piggybacking on their due diligence, know-how, and deal terms. (See more on tag-along strategy in the note section.)

2) Picking the Founder(s)

“An entrepreneur is someone who does more than anyone thinks is possible with less than anyone thinks is possible.” John Doerr

If you were to place a bet on a horse race, would you bet on the jockey or the horse? At an early stage, you do not have the horse, so you might as well be good at picking the jockey.

Identifying the right founder(s) is probably what you should weigh more heavily when making an investment decision, especially in the company’s early stages. At the seed stage of a company, you have little or no user data, revenues, margins, or information on how the proposed product interacts with its target market. Below is a list of the most important traits for a founder to have, according to the best Venture Capitalists (VCs) and entrepreneurs.

Founder traits: What are you looking for?

A clear and concise communicator: Depth of understanding and clarity of thought when pitching the opportunity to stakeholders.

A talent magnet: It takes a team to win: “We believe that ideas are easy, execution is everything, and in anything worth doing, it takes a team to win.” John Doerr

Moves fast: They iterate very quickly. The ones that do a release every two years fail. Former CEO of Intel, Andy Grove stated: “Execution is what matters most.” Can you Get It Done? Can you ship on time? CAN YOU SHIP ON TIME?

A great storyteller: You want someone who is more than a salesperson. You want him to take you (and other stakeholders) on a journey.

Accomplishes a lot with a little: This cannot be repeated enough; you are looking for someone “who does more than anyone thinks is possible with less than anyone thinks is possible.” John Doerr

Makes something people want: The founding team starts something so interesting that people would want to help them for free!

Determined and committed: “What matters most is determination. You’re going to hit a lot of obstacles. You can’t be the sort of person who gets demoralized easily.” Paul Graham

Long-term thinker: “Even decisions that maybe they shouldn’t care that much about early on, they fix it because they are not building a house, they’re putting bricks in the foundation of the skyscraper, at least in their minds.” -Naval Ravikant

Integrity: Last but not least, you want someone with good values. Warren Buffett jokes that he likes to work with people who are smart, high energy and high integrity. If the person does not have high integrity, it is better that they are stupid and low energy. If not, you have a very smart crook around you who can find ways to cheat you with unstoppable stamina.

Warning Traits:

Too Perfect: Paul Buchheit, a Y-Combinator (YC) partner, says that he “is skeptical of people who have not fucked up and have perfect grades. These are people who have never failed. They will take an early exit to add it to a resume and look for a safe job.”

Should you invest in single founders?

Statistically speaking, no! “Having two founders, rather than one, significantly increases your odds of success as you will raise 30 percent more money, have almost 3X the user growth, and are 19 percent less likely to scale prematurely.” (Source)

Is there a magic number for a winning founding team? It’s a trick question. It is not about people but “personas” that have specific attributes or skill sets. What personas are we looking for then?

3Hs: The hacker, the hustler and the hipster (Designer)

“There are three personas that should be present in every startup team: the hacker is all about tech; the hipster cares for the product, and the hustler is the commercial one. If you want your company to be a baby unicorn you need those skills in your team. That’s why we don’t invest in single-founder companies: the one person who can embody all these characteristics is rare, but a founding team of two may do the trick – if they cover all three personas.” (Source)

Founder Divorce:

One of the most significant risks in a startup’s early stages is co-founders who do not get along. As an investor, you do not want to be the divorce lawyer. About 20% of companies funded by YC have at least one founder who leaves (Source). These are venture-backed startups graduating from one of the best accelerators in the world. The number could be even higher for startups that do not go through prior rigorous sourcing and consequent training.

Investor Beer Test:

If you are going to participate in an early-round investment where there is an expectation that you will be working closely with the startup, ask yourself, do they pass the beer test? Can you have a beer with this person every week for 10+ years? If the answer is no, then they do not pass the beer test. The average amount of time it takes a company to go public is between 10 to 16 years; this time frame is longer than the average marriage (8 years in the US). If they do not pass the beer test, I would not recommend having substantial participation in the company this founder(s) owns and even less, considering them as a co-founder.

In conclusion, at an early stage, you are mostly betting on a team of founders who have relentless fire in their bellies and as John Doerr said they are a team of people who can “do more than anyone thinks is possible with less than anyone thinks is possible.”

3) The Idea: Start with the problems, not the solution

“Start something so interesting that people want to help you for free.”

The idea matters. Don’t believe me? Go back in time to when you tried to influence a group of people to do something unconventional. Remember the upward battle it was to alter people’s inertia, especially when you did not secure full buy-in from the group? But suddenly, you changed your pitch, and everything clicked into place. Some people in the group even started to appropriate the idea as if it were their own, and it unconsciously produced a downward shift in momentum. The group just got it. Better yet, they started to promote it. For startup ideas, this happens as well, and some ideas are more prone than others to scale.

What are you looking for when analyzing the idea being pitched by the founding team?

a) Can the founding team communicate the idea clearly? Sam Altman, president of Y- Combinator writes: “Ideas, in general, need to be clear to spread, and complex ideas are almost always a sign of muddled thinking or a made-up problem. If the idea does not excite at least some people the first time they hear it, that’s bad.”

b) Is the founding team the target user? Altman also states: “In the best case, you yourself [the founding team] are the target user. In the second-best case, you understand the target user extremely well.”

c) Is the team is building something people want? The fundamental problem with most startups is making things that people don’t want or don’t care about. Instagram founder Kevin Systrom observed, “The App Store is 90% full of solution-based apps … But do they solve a problem?” He learned this lesson from his first startup Burbn, where he started at a solution and worked back.

d) Are they building something that people are already getting for free? If so, don’t go into a market where people are getting solutions for FREE. Billionaire investor Chris Sacca advises: “Solve problems where people are already paying for solutions. I failed miserably trying to ‘invent’ a piece of software in a space (analytics) where people were mainly using free apps. It wasn’t the world’s worst idea, but convincing people to pay for something that they don’t pay for already is much harder than you’d think.”

e) Is the team willing to kill or change their original idea? Don’t fall in love with your idea: “It’s important to let your idea evolve as you get feedback from users. And it’s critical you understand your users really well—you need this to evaluate an idea, build a great product, and build a great company.” Sam Altman

f) Does it have monopoly potential?“Look for businesses that get more powerful with scale and that are difficult to copy.” Sam Altman

g) Is it a truly new idea and not a derivative of an existing idea? “We greatly prefer something new to something derivative. Most really big companies start with something fundamentally new (an accepted definition of new is 10x better). If there are ten other companies starting at the same time with the same plan, and it sounds a whole lot like something that already exists, we are skeptical.” Sam Altman

4) The Market & Potential Growth

There is a big debate between the great VCs of what is more crucial when analyzing an investment opportunity: the team, the idea, or the market? For Don Valentine, founder of Sequoia Capital, one of the most prestigious venture capital firms in the world, the potential of capturing a large market was the primary driver in his investment decisions: “I like opportunities that are addressing markets so big that even the management team can’t get in its way.” While the most important element at an early stage of a startup is debatable, the market potential is probably the most important in later stages. Counterintuitively, the first step is to start small.

Start small and monopolize a small market:

Legendary investor and entrepreneur Peter Thiel advises starting small and monopolizing a small market. A founding team must be relentless and obsessed with talking to users. They should focus on building something a small group of people loves rather than a product that many people like. Most startups do not fail because of competition; they fail because they do not make products that people love.

Growth Potential:

Sam Altman, in his Startup Playbook, addresses this point very succinctly: “If a company already has users, we ask how many and how fast that number is growing. We try to figure out why it’s not growing faster, and we especially try to figure out if users really love the product. Usually, this means they’re telling their friends to use the product without prompting from the company. We also ask if the company is generating revenue, and if not, why not.” (Source) It is imperative to think about the growth of the market in 10 years. It can be a small but rapidly growing market that can grow into a bigger market. Think uber, at first, they went after town cars, limousines and upscale transportation. They later grew into competing with taxis, now they compete with short term rental services, or even with a household cars when thinking of purchasing an extra vehicle for the family.

Evaluate three important types of growth:

Unlike Thomas Jefferson’s scripture in the US. Declaration of Independence, not all growth should be treated equally. Analyze how your prospective investment company is acquiring their customer and segment how they are growing. There are three main forms of increasing your user base.

Sticky growth: customer lifetime value (CLV) is increasing

Viral growth: Create a remarkable experience + have a great referral program

Paid growth: makes sense if your customer lifetime value (CLV) is larger than your customer acquisition cost (CAC)

Paid growth should not be a startup’s primary source of growth. If customers do not love the startup’s product and are not spontaneously telling their friends, the startup’s focus should not be on optimizing their paid growth initiatives but on optimizing their product experience.

Real trend vs. a fake trend?

Some companies get a lot of buzz because of celebrity endorsements, savvy marketing campaigns that generate word of mouth recommendations, or when they do something that is so outrageously different that it generates a lot of chatter. However, talk does not equate to action or frequency of use. Look under the hood and evaluate users’ actions. Are people actually using these products, or are they just talking about them? Dig deeper and confirm if people are genuinely paying for a particular product, estimate the frequency of use, and find out if they would be disappointed if the product or service in question ceased to exist.

Market growth and size:

Sam Altman points out that, before investing, he asks key questions about the market: “How big it is today, how fast it’s growing, and why it’s going to be big in ten years. We try to understand why the market is going to grow quickly, and why it’s a good market for a startup to go after. We like it when major technological shifts are just starting that most people haven’t realized yet—big companies are bad at addressing those. And somewhat counterintuitively, the best answer is going after a large part of a small market.” (Source).

As Altman highlights, the trick is to spot technological shifts and to identify markets in their infancy, before they become huge. “Great markets make great companies. We're never interested in creating markets—it’s too expensive. We’re interested in exploiting markets early.” Don Valentine

5) Moats and Scalability: How do you defend your fortress?

First of all, what is a moat?

“The term “moat” was popularized by Warren Buffett, and it generally means the durable ability for a business to increasingly dominate a market without losing profits to competition. There are different types of moats, and they become apparent as businesses scale. For example, some of the most desired modern moats are: 1) monetizable integrated network effects (Facebook), 2) ascending data leverage (Google), and asset-light purchasing power (Amazon) 3). The best moats compound—meaning all additional investments into building them generate logarithmic returns.” (Source).

*Assumption: The hierarchy of the moats listed is for startup companies that operated in venture-friendly markets such as the US. In other words, markets that favor private enterprises as opposed to government-controlled venture back entities.

a) Network effects:

What are Network effects? “Best described by Metcalf’s law, your product or service has “network effects” if each additional user of your product accrues more value to every other user. Messaging apps like Slack and WhatsApp and social networks like Facebook are good examples of strong network effects. Operating systems like iOS, Android, and Windows have strong network effects because as more customers use the OS, more applications are built on top of it.” Jerry Chen, partner at Greylock (source).

Network effects being at the top of the list might sound counterintuitive, but it is one of the most powerful moats in the life of an early-stage startup. You can start by controlling a small market as Facebook did at the beginning when it only allowed access to Harvard students. Facebook gradually expanded to other campuses as they hit a critical mass of users.

b) Switching costs, data use lock-ins:

Switching costs increase with the amount of data that is stored and locked within a product. For example, if all of your contacts or deals pipeline are programmed in an application such as Salesforce, and the export process is not seamless, you’ll likely think twice before switching from your Customer Relationship Manager (CRM). The defensibility of a product is also correlated with the number of users on the platform and the amount of training and adoption you have invested to use a tool. If your entire company has been using and collaborating on Zendesk for a few years, it might not be that easy to change your ticketing software.

c) Brand or mindshare: Own a Category

A great brand objective is to own a category. Once a company becomes top of mind for its customers, it is possible for the consumer to not even look for alternatives. Do you remember the last time you used Bing for search or asked your friend to take an Uber to your house instead of asking him to use a car-sharing app?

“With each positive interaction between your product and your customers, your brand advantage gets stronger over time, but that strength can deteriorate if your customers lose trust in your product.” (source)

d) Distribution channels: Value Added Resellers (VAR)

If you have thousands of partners who have been trained to sell your product and make considerable money doing it, this can be another very valuable moat. A VAR is a value-added reseller of a company that resells software, hardware, or networking products, and provides value beyond order fulfillment. Hubspot has this partnership with thousands of marketing agencies, WordPress has it with freelance web developers, and SAP does too with robust companies that resell their software and offer integrated solutions.

e) Platform or marketplace

A good example is the Salesforce.com platform. The large number of applications that integrate with Salesforce make Salesforce one of the most comprehensive CRM solutions on the market and give the company a huge competitive edge. This is a classic example of a virtuous circle: more customers attract more developers, which in turn attracts more customers.

f) Superior technology, protected IP, exclusive licensing private or government.

Another way to prevent competition is to have a unique technology that is very difficult to copy, which could be patented. Patents for new drugs in the pharmaceutical industry are an excellent example of protected intellectual property (IP).

Proprietary software are methods where most technology companies begin. These trade secrets can include novel solutions to hard technical problems, new inventions, new processes, or new techniques, and later, patents that protect the developed intellectual property. Over time, a company’s IP may evolve from a specific engineering solution to accumulated operating knowledge or insight into a problem or process.

g) Big Data or data network effects

“Machine Learning (ML) products become better as they ingest more data. If you own the data that is required to train a Machine Learning powered product, and nobody else does, chances are high that greedy incumbents won’t be able to build a product as great as yours.

If you have tens of thousands of customers, the massive amounts of data created by your customer base might allow you to draw insights that you can then give back to your customers. Zendesk’s benchmarking reports come to mind as an example.” Louis Coppey (source).

h) Economies of scale

“Last is Economies of Scale (which is different from a network effect). Once startups get bigger, they lower their break-even points, increase their bargaining power to increase prices, decrease costs, and protect themselves from new envious startups willing to enter the space. Did you ever think about starting a book marketplace?

The bigger you are the more operating leverage you have which lowers your costs. SaaS and cloud services can have strong economies of scale: you can scale your revenue and customer base while keeping the core engineering of your product relatively flat.” Louis Coppey (source).

Take away:

Can your prospective company successfully build any of these types of moats? If you do not have a defensible moat and competitors have the capabilities to produce the same product/services at the same cost, they can then reduce their gross margins at the same rate as you. Having access to the same suppliers and technology, at the same cost, reduces your competitive advantage to focus on operational efficiencies, which are dependent on the management team. You want structural competitive advantages that, with a suboptimal management team, can still defend your margins. As Warren Buffett once said, “I try to invest in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.”

6) Unit Economics: Your Scalability Lever

a) What is Unit Economics?

“Unit economics, in general, is a profit/loss calculation per customer. This is an aggregate indicator that determines whether there is a financial sense in scaling the project and where the project has a break-even point.” (Source).

b) How do you identify it in your business? What is your Unit of Value?

“Define what it is you’re building that has economic, not emotional, value. Coca Cola’s unit of value is a can of fizzy drink; a movie theatre’s unit of value is a seat at an event; Google’s unit of value is a paid click (CPC, CPA or CPM); and Uber’s unit of value is a paid ride or delivery.” (source).

All companies have a unit of value. As an investor, it is important to understand what is the unit of value of your prospective company.

C) How to calculate your Unit Economics gross profit %?

“All units of value have a sale price, a cost of sale, and a gross profit. These makeup unit economics. Uber charges per mile for a ride, the driver gets a percent of that charge, and the app itself has some costs associated with it (COGs/COS/CAC). If the sale price per mile is $1, and the cost of sale is $0.50, then the gross profit is 50%. Your operating income (cash needed to run the business) comes from this gross profit, as does your actual profit (net earnings). This can be calculated per business model or the unit you sell.” Keith Teare (Source)

D) What is an optimal Customer Acquisition Cost (CAC) to Customer Lifetime Value (CLV) relationship?

The answers:

A payback period that is less than 12 months and

A CLV/CAC ratio that is ideally higher than 3 meaning that for every 1 dollar you spend to acquire a customer (CAC) you should be getting 3 dollars back (CLV).

To calculate CLV: CAC Ratio go to the following website: Link

7) Business and Investor Optionality

Optionality

It’s all about increasing optionality! Impression Ventures’ blog sums it up best: “Optionality is the value of additional optional investment opportunities available only after having made an initial investment. In other words, optionality is the sum value of all options created by a decision.If a decision creates no new options, it has no net-new optionality. If a decision forces you to one outcome, it has zero dollars of optionality and in fact, has net-negative optionality. The best decisions create net-new optionality. Those are the nice juicy decisions that lead to great financial outcomes.” (source).

Two major categories increase optionality when investing in startups. One is taking into account if the business model itself can structurally create more options, and the other is for the investors to have more options in terms of how he finances the startup. The first is more important because, if the business as a whole does better, it creates more favorable opportunities for all stakeholders in the company.

Financial optionality: for the business

A business can increase its optionality when one or more of the following three criteria are attainable:

Reaches profitability quickly (Ramen Noodle Profitable)

Is an attractive investment for multiple companies

Has the potential for IPO (due to size, revenue growth, and other factors)

*In the note section there are additional references and graphs that better explain the concept of Ramen Noodle Profitable, how to increase the odds of becoming attractive to multiple companies for acquisition, and how companies can position themselves to have a higher potential for IPO.

Financial optionality: for investors

In terms of optionality for having a potential claim on the future cash flows of a company, you can fund a company by using financial instruments that give you multiple options in terms of rights and provisions. Such options include issuing convertible notes, which provides you with the possibility of converting debt into preferred stocks and/or other rights that protect your downside. (More information on convertible notes is covered in the note section.) As a venture investor, it is advisable to only enter into agreements with financial instruments such as preferred stock or convertible notes that may later convert into preferred stock.

Preferred stock

Why preferred stock instead of common stock? As opposed to common stockholders, preferred stockholders can negotiate different rights and provisions that can protect the investment. The following are the most important to negotiate, especially if you are a minority stockholder.

Liquidation preferences

“The preferred stockholders will have the option of taking their cost out or sharing in the proceeds with the founders as common stockholders. What this means is that if the value of the sale of the company is below the valuation, the preferred investors paid, then they will get their money back. If the sale is for more than the valuation the preferred investors paid, then they will get the percentage of the company they own.” Fred Wilson (Source).

Right to participate in future rounds

Pro-rata rights: a right to participate in future rounds to maintain percentage ownership.

Right of first refusal: on all transfers of common stock. If the company elects not to exercise its right, the company shall assign its right to the Investors.

Co-sale right: the founders may not sell, transfer, or exchange their stock unless each investor has an opportunity to participate in the sale on a pro-rata basis.

Anti-dilution right: Right to adjustment in the purchase price to reflect sales of stock at lower prices.

Information rights

An example of a standard clause regarding information rights: “Company shall deliver to the Investor the Company’s annual budget, as well as audited annual and unaudited quarterly financial statements. Furthermore, the company shall furnish a report to each investor comparing each annual budget to such financial statements. Each investor shall also be entitled to standard inspection and visitation rights.” Brad Feld (Source).

Shareholder agreement

Make sure that there is a sound shareholder agreement in place that aligns the interests and incentives of the companies, shareholders, board members, and management. This agreement is especially important when key people have multiple roles. An example is a founder being the CEO of the company, having a board seat, and at the same time being a major shareholder. This agreement should be used as an instrument that favors and aligns all shareholders, at the same time, provides checks and balances between management and shareholders.

8) Exit Strategy: 3 Questions to Ask Yourself Before Investing

To start with the end in mind, you should ask yourself three questions which are not very romantic. They can even be a buzzkill for the passionate entrepreneur or enthusiastic investor who is enthralled with the startup they are endorsing. Nonetheless, someone has to ask these questions, which might sound unsympathetic, but ironically they help all stakeholders involved in the long run.

In plain English, these are the three questions to ask yourself before investing: 1) How much money should I make and in what period of time? 2) Does this startup have the potential to generate the expected returns needed for the risk that is being taken? 3) If this turns out to be a good investment, should I sell a portion of my stocks to secure some profits?

How much money should I make and in what period of time?

Purely based on expectations of returns and given the risk you are assuming with an early-stage startup, you are looking for an Internal Rate of Return (IRR) return much higher than what you would get investing in an S&P 500 index fund which averages 8% IRR (Source). The ideal startup performance is more than 25% IRR. This means more than 3x (3 times your money) in 5 years or 10x in 10 years. Below is a graph that outlines the math more clearly.

To be blunt: if you invest in a fund or directly with an entrepreneur, there should be a clear expectation that you are seeking 25%+ IRR on your investment, given the risk that comes with investing in startups. In venture capital funding, doubling your money in seven years is not something to celebrate in a mere expectations perspective (10% IRR). For that same return, you should have stayed at home and invested in an S&P 500 index fund, which is substantially more liquid and has by far a better risk/return ratio than a startup that is promising a 10% IRR.

Does your startup have 25%+ IRR potential?

Now that you have a clear goal of expecting 25%+ IRR on your investment, what companies do you send a check to? In essence, to a company that has the potential to be radioactive in terms of growth; a company that is growing much faster than its peers in a given category (private or public). But what revenue threshold are we talking about? Ideally, a company that can reach $50 million in revenue in less than 6 years?

What is one of the best indicators that this company is on the right track? Your monthly or weekly revenue growth rate! To give you a real-world example: Facebook grew 2256% in terms of revenue in its second year of operations. Yes, revenue (not just users) it exploded from $382K to $9M. In year three it grew 433% from $9M to $48M, reaching the $50M revenue mark in almost 3 years.

Take aways:

Before investing, study a company’s weekly and monthly growth rates and benchmark that growth with other companies at a similar stage. If the company is not growing as fast in terms of revenue as its peers in the same industry or stage, investigate if maybe the company is prioritizing other initiatives, such as building a stronger defensible moat, which will guarantee faster growth or better margins than their industry peers. But if they have a slower revenue growth rate due to operational inefficiencies or poor market receptibility to their offerings, consider investing in another startup or asset class. For a revenue growth benchmark chart, see the appendix section.

Exit strategy: Should I wait until the IPO to cash in all my earnings?

In most cases, as a minority shareholder, you have little-to-no influence in pushing an exit. Things get even tougher if the company you invested in is running out of cash or has flat growth. In this regard, there is not much to talk about, just hope the company makes a turnaround in terms of growth, finds an acquirer, or restructures and becomes profitable.

On the other hand, things may get a bit more interesting if you manage to invest in a radioactive company in terms of growth. Why? A lot more options appear. Here is where it pays to have clarity on your % IRR end goal. If you have a buyer who is willing to buy a portion of your stocks at 5X of what you paid in less than 2 years (124% IRR) would you accept? Maybe. This advice might not seem sexy, but consider the possibility of selling at least your cost of entry, or even just taking some profits off what you invested initially. Below is a chart of the best performing US venture capital funds based off net IRR returns for their investors.

Top Performing North America-based Venture Capital Funds

Take Aways:

Notice that from 2003 to 2015, the best historical return was 67% IRR. If you have a 124% IRR on your hands, don’t play the eccentric, illuminated-genius card and keep holding all the stock in your hands. Sell and lock in a portion of those returns—chances are, you probably got lucky anyway. To invoke Charlie Munger’s favorite quote in this situation: “Avoiding stupidity is easier than seeking brilliance.”

Conclusion:

In Mario Puzo’s book The Godfather, Micheal Corleone says to Kay Adams, his then fiancé: “I don’t trust society to protect us, I have no intention of placing my fate in the hands of men whose only qualification is that they managed to con a block of people to vote for them.”

What Micheal was trying to portray to his fiancé is that you should not put your fate in the hands of others. Ultimately you have to take responsibility for the investment decisions you make. Sit down and create a checklist. Don’t know where to start? Start by taking tips from the best, and make iterations until that list becomes your own. After you make your checklist and have an investment thesis, do not break your own rules. This may sound rigid, but when it comes to negotiating a deal, there are “con men” who are geniuses in selling and raising money. If you do break one of your rules, there must be a far greater compensation tradeoff than the risks you are willingly taking.

As an endnote, do not start investing, start analyzing deal flow. Research investment opportunities. Study pitch decks, talk to other entrepreneurs, and only after examining dozens of deals, start making very small bets. The greatest reward you will receive is in the process of studying different company’s strategies, from deeply considering their potential outcomes and coming up with your own insights. These critical thinking exercises and personal insights are your most significant rewards, distinct from the financial outcomes that arrive later if you are correct.

*If you are an investor who is interested in co-investing with us, or you are an entrepreneur looking for funding. Go to the about page and fill out the form. If you are just starting, we can also help you with your pitch deck through the partner companies we work with.

Special thanks to: Luis Cisneros, Andres Brillembourg, Maria Fernanda Mendez and Cristina Schaver for reading drafts of this article.

Note Section:

Tag-Along Strategy: (Mentioned in the Introduction)

Endeavor Catalyst, our rules-based fund, co-invests in Endeavor Entrepreneurs raising rounds of minimum US$5M in equity capital led by qualified institutional investors. Our fund invests up to 10% of each qualifying round, currently capped at $2M per company. As of June 2019, Endeavor Catalyst has co-invested in over 115 companies across 25 markets with six full exits and four “unicorns” in its active portfolio. Learn more about Endeavor Catalyst here. Read: https://endeavor.org/approach/catalyst/

Reasons Why Startups Fail:

74% of High Growth Internet Startups Fail due to premature scaling, Premature scaling means spending money on marketing, hiring, etc. either before you found a working business model (you acquire users for less than the revenue they bring) or in general spending too fast while failing to secure further financing. (Source).

Startups that scale properly grow 20X faster (Source).

62% of Startups fail due to co-founder conflicts (Funders and Founders)

52% are less likely to scale prematurely if the startup has “pivoted” once or twice (Quora)

42% identified “lack of a market need for their product” as the single biggest reason for their failure (Forbes)

30% fail because their management was not experienced enough to handle finances, hiring and marketing (Entrepreneurial Insights)

Founder Statistics:

80% of successful Startups have multiple founders (VC Josh Hannah)

Although founders of previously successful businesses have a 30% chance of success with their next venture, founders who have failed at a prior business have a 20% chance of succeeding versus an 18% chance of success for first-time entrepreneurs. (Source)

The average age of people who founded SUCCESSFUL HIGH GROWTH STARTUPS is 45 years old. (Source)

Interestingly, when you analyzed the outliers/exceptions to the 45-year-old rule to the iconic founders that started in their twenties such as Bill Gates, Steve Jobs, Jeff Bezos, or Sergey Brin and Larry Page, the growth rates of their businesses in terms of market capitalization peaked when these founders were middle-aged.

Two founders, rather than one, significantly increases your odds of success. You will raise 30% more investment, grow your customers 3 times as fast, and will be less likely to scale too fast.

Over 52% of founders of Valley start-ups are non-US (Source).

Where does the funding come from?

1% comes from VC firms (Entrepreneur)

3% comes from Crowdsourcing (Entrepreneur)

24% comes from friends and family (Entrepreneur)

41% loans or lines of credit (Entrepreneur)

82% are self-funded (Entrepreneur)

Pro-tip: Don’t ask investors who say no for introductions to other investors. That will in many cases be an anti-recommendation. -Paul Graham (Source)

Unfair Advantage:

Founders with breakout startups often have an unfair advantage. Google had their Stanford connections, filled with talented algorithm-writing engineering geniuses. Facebook launched while Zuckerberg was still a student at Harvard, and they used their understanding of campus culture and [access to] directories to figure out the dynamics of building online social networks that scale. Mark Pincus launched Zynga with a multi-year cross-promotion deal with Facebook, which allowed Zynga to tag along with Facebook as it grew at an astounding rate. Mary Gates was on the board of United Way with the CEO of IBM, which led directly to IBM hiring her son Bill’s new company, Microsoft, to build the operating system for their first personal computer (Source).

The way to succeed in a startup is not to be an expert on startups, but to be an expert on your users and the problem you’re solving for them. (Full Article)

How to create financial exit optionality and become more attractive to future buyers:

Profitability: Reaching and maintaining profitability fast gives you the luxury of not needing outside capital to survive. Strive to reach what Paul Graham calls Ramen Noodle Profitable: (Source)

Create a list of potential acquirers, divided into Customers, Investors, and Partners: Customers: List your biggest customers. Investors: Besides Angles and VC, try to have corporate investors in your capable, that might acquire you in the future. Partners: Have a list of your biggest partners, especially partners that could benefit from a merger. Important: Nurture a working relationship where you discuss the possibility of acquisitions with all three stakeholders openly. (Source).

Companies Buy Engines, Not Heroes: It is important to build a repeatable process that anyone can run. If you build an engine to grow revenue, then an acquirer will see that they can just add more fuel to the engine to accelerate growth. Build systems and processes for how you grow your business. Systems drive value since they are not dependent on one individual. (Source)

What drives a premium IPO valuation?

a) Size. The sweet spot for IPO valuations is occupied by midsize companies, not the largest issuers. Midsize companies—with a market cap of €300 million to €1 billion—enjoy the highest likelihood (64%) of receiving a premium valuation. The smallest issuers (market cap of less than €50 million) have the lowest likelihood (45%). The largest issuers (market cap exceeding €10 billion) also show a very low likelihood (20%) of receiving a premium valuation, reflecting the fact that very large IPOs often are priced conservatively, or even at a discount, to ensure successful share placements. We also found that companies with a large number of employees compared with their industry peers are less likely to receive a premium valuation. What drives a premium IPO valuation: (Source).

b) The 2018 Boston Consulting group study "confirmed that some intuitive factors, such as strong revenue growth and above-average margins, are highly influential. But some less obvious factors, including organizational complexity, leverage, and expected dividend yield, are equally important. " (Source)

What Drives Down Rounds?

Down rounds by Natasha Ketabchi:

"Down rounds basically occur for private companies for the same reasons they do for publicly traded companies:

Failure to meet investors’ earnings targets: If a company fails to reach the necessary milestones, investors growth forecasts will have to be revised downwards, and with them the company’s valuation.

Deteriorated competitive environment: If new competitors have emerged for a company, the expectations of its ability to grab market share will also weigh on valuation.

Tightening of general funding conditions: This factor is sadly completely outside of a company’s control - lower investor appetite for private company equity will decrease valuations for everyone(source)".

Implications of a down round by Natasha Ketabchi:

"The main implication of a down round is the triggering of anti-dilution protection, which means that when shares get sold at a lower price than an investor had originally paid for them, the investor will be diluted less than the other parties.

Other important secondary implications are negative signaling to the market and investors, a loss of trust and confidence in the company, lower motivation, and control on behalf of the founders and management, and a negative hit to employee morale(source)".

Pitch Deck Stats:

Average Slides per Pitch Deck: Seed Stage 18 Pages. Series A 24 pages (Source).

Meetings and time to raise: Average of 40 investor meetings and 3 Months to close ( Source: techcrunch)

Average time investors spend looking at pitch decks: 3:44 Minutes. ( Source: techcrunch)

There wasn’t really any correlation between more meetings and more funding. If you contact more investors, you’ll get more meetings. But there is no correlation between the number of investors contacted and the amount of money raised. (Source).

Then, seed funds can move faster and provide more money than angels. The average amount of time it took to raise from firms was four weeks shorter than the amount of time it took to raise from angels. Also, rounds that were led by firms tended to be 36.8 percent oversubscribed while angel rounds were 18.9 percent oversubscribed. (Source).

The most important pages are the financials, team and competition, according to how long investors study them. (Source).

It’s better to go find firms that are already aligned with what your company does and target them first.

CARTA CEO source Here..

Investment Checklists:

Fabrice Grinda: Link

Tim Ferris, Tool of Titans (Page 254)

James Altucher (Seccion H): Link

Kogito Ventures ( Startup evaluation process seccion): Link

Other Cool Facts:

“Software alone is a commodity,” Wilson wrote in a 2014 blog post. The only way to build a defensible business model, he argues, is to own a network of users, transactions, and/or data. (Source)

Startup Revenue Benchmarks: Link

Fools Rush In: 37 Of The Worst Corporate M&A Flops: Link

Your Startup Has a 1.28% Chance of Becoming a Unicorn (Source)

Margin of Safety: "To bastardize Warren Buffett’s bridge analogy regarding the margin of safety: We want to invest in founders that can lift the weight of the world, but really only need to lift the weight of one difficult startup business. We will almost certainly be fooled both positively and negatively by prices, products and markets, but we must do our best not to be fooled by teams, because they’re the only margin of safety we have". - Doug Clinton (Source).

Readings:

Overall information on Entrepreneurship:

Y Combinators /Sam Altman Reading List: Link

Paul Graham’s article on Growth: Link

Before the Startup (Counterintuitive points) by Paul Graham: Link

How to Raise Money by Paul Graham: Link

How to understand the viewpoint of Investors by Paul Graham: Link

How to make wealth by Paul Graham: Link

Investing Benchmarks:

40 Of The Best VC Bets Of All Time: Link

The Path To IPO, see how these startups grew into public companies: Link

Unicorn Tracker: Link

Valuation & Returns:

How Investors Value Startups: Link

How investor Value Private companies: Link

Exit Strategy/ Why VC’s seek 10x returns: Link

Angel Investing: (Preseed and Seed)

Jason Calacanis on questions to ask before you invest in a founder: Link

Legal:

Convertible Notes: Convertible Notes | Seed Financings

Startup documents: YC Documents

Philosophical:

Futuristic view on Tech and Software by Marc Andreessen: Link

Technical and Management Debt concept Mike Maples/ Tren Griffin: Link

Podcast: Naval Ravikant interviewed by Shane Parrish. Title: “The Angel Philosopher" Link

Podcast: Sam Altman interviewed by Reid Hoffman Link

Courses:

Y-Combinator: How to Start a Startup

Graphs:

VC Funding Stages

Source: Link

VC Valuation Method

Source: Link

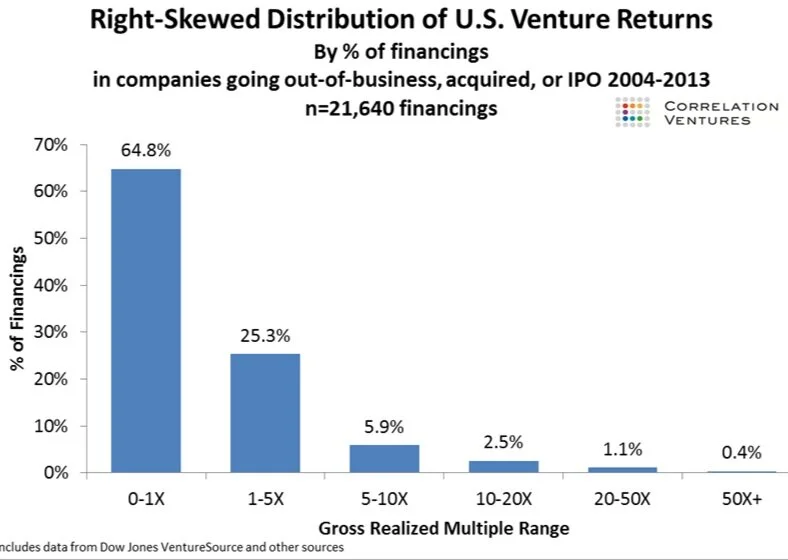

Return Multiples

Revenue Benchmarks:

Bonus Section: Deal Flow Strategy

This post ran way too long, but I wanted to leave this short bonus section at the and just in case you kept reading. The quality of investment may be determined by the quality of your deal flow.

Here is a list of a few strategies:

Track successful entrepreneurs, talent attracts talent. And if they are on the verge of starting another company, double down on their next endeavor.

Co-invest and create relationships with investors you admire, and like their thinking. This applies to past co-investors whom you admire and like working with.

Get introduced to the founders of your co-investors portfolio companies

Meet other super connectors, which are not VC's or founder's: It might be a super angel investor, an attorney that works with several successful entrepreneurs, Business Coaches, Business advisors, etc...

Start writing about your investment thesis or create content that helps the entrepreneurship community

Create a coworking business and invite other startup companies, this is what we did in Cokrea.co

Offer mentorship programs and collaborate with other accelerators

Build a Brand that positions you as a startup propeller

Build proprietary software that tracks data and produces insights to the venture business ecosystem. Here is an article related to companies and funds who are using technology to optimize deal flow: Link

If you are an investor who is interested in co-investing with us, or you are an entrepreneur looking for funding. Go to the about page and fill out the form. If you are just starting, we can also help you with your pitch deck through the partner companies we work with.